The business of producing food has never been a piece of cake (apart from growing cress on a damp kitchen towel), particularly for farmers. It’s extraordinarily challenging when tragic wars are bringing upward pressure on the costs and even availability of key inputs, such as energy, fertiliser, feed costs and ocean freight transport (only the most perspicacious business planner would’ve put simultaneous problems in The Red Sea and The Panama Canal down on the “must watch as immediate risks to my business” list). Then, there’s the excruciating double whammy of a wet and warm El Niño period exacerbating the advance of the frightening global climate change era (N.B. era not period). To make things even worse, some governments have taken the moment to implement agricultural policies (well-intentioned but, arguably, ill-timed and/or inept) to address a plethora of issues such as: across the EU and the UK, legions of farmers squeezed by economic pressures and outraged by perceived over-regulation largely relating to environmental policy, feeling let down by free-trade agreements, and the threat of the removal of subsidy on farm fuels. In David’s “home country” Wales, farmers have been incandescent over The Welsh Government’s proposed policy to require farmers to bring their existing tree and woodland cover up to 10% of their total farm acreage, as have Dutch dairy farmers threatened by their government wanting to “force purchase” farms to reduce the nitrogen pollution impact of intensive livestock production. Welsh farmers made their point by placing thousands of pairs of wellington boots (“wellies”) on the steps of The Welsh Parliament, whereas EU farmers showed how effective a few hundred tractors blocking the roads to large cities can create traffic chaos.

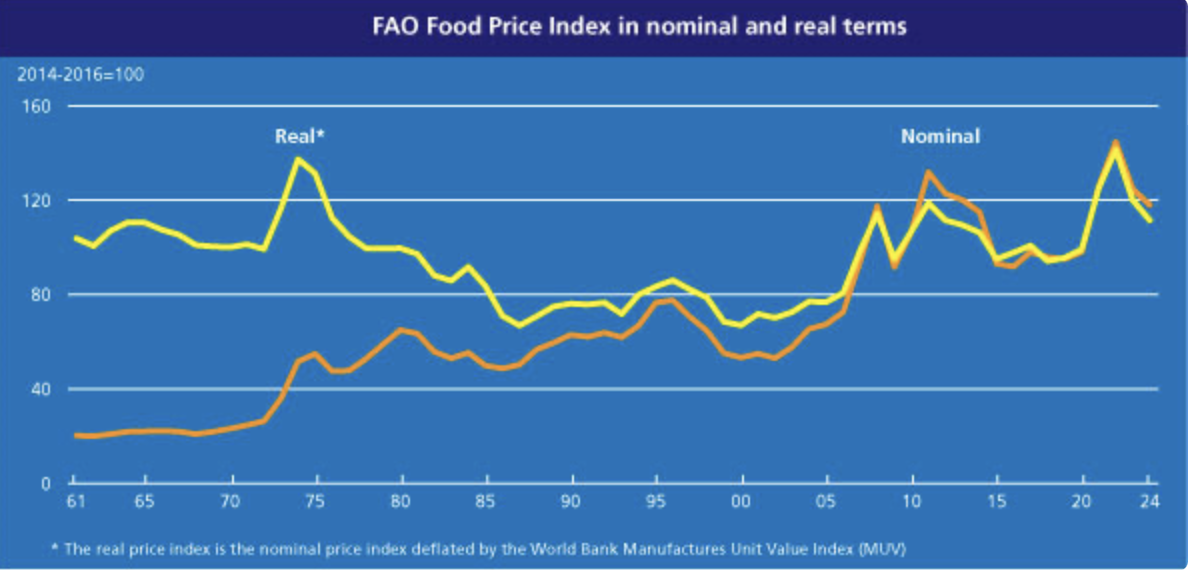

Currently, there’s not a lot of happiness about! Food consumers aren’t over the moon. Food prices rose by only around 2% between May 2023 and March 2024, hurrah! But food prices rose 22% between March 2022 and May 2023. So, consumers have seen their food bills rise by close to 25% since the pre-Covid period, whilst many farmers have seen their net incomes ravaged. Those at the beginning and the end of the food chain blame those in the middle. It was ever thus in a cost-of-living crisis! “Big Food” takes the rap – i.e. large supermarket chains and the mega-branded international food processing companies. One manifestation of the rap is the launch of government enquiries into profitability in the food system with the intent of identifying villains. There’re dozens of such enquiries about, not least in countries where a few supermarket chains (e.g. 2 in each of Australia and New Zealand) have a huge, combined grocery market share. The findings? In competitive grocery markets which are in a notable food price inflation period, supermarket chains are not shown to be iniquitous profiteers. Oh, boo! In the UK, the Competition & Markets Authority (CMA) report that aggregate operating profit for the retailers’ grocery businesses between FY2019/20 and 2022/23 declined from around 3.3% to 1.9%. It may be reassuring for financially literate consumers that their grocer makes less than 2p in the £ profit but it’s cold comfort for a supplier to that grocer who’s been squeezed into supplying the grocer at a loss such that the supermarket chain can be competitive with an on-the-loose hard discounter! There’s been a lot of that about. Mind you, for those in the food industry, for our final customers, buying food isn’t an option, it’s a prerequisite for the life of the family. You can put off buying the new sofa but, one way or another, you’ll have to acquire food.

It can be tough for one and all in a difficult inflationary period and excruciating for some! Low-income consumers, for a start. Household income polarisation in the UK (and, to a lesser extent, in the USA) has increased over the past 50 years or so. Rampant food price inflation hurts poor households – the lowest income households in the USA spend 30+% of income on food (say $6,000/p.a. total), whereas the top group spend 5% of income on food (say $17,000) – the percentage figures are not dissimilar in the UK. It’s a salutary reminder that there are “income haves” and “income have nots” and, also, explains why premium retailers such as Marks & Spencer (M&S) and Waitrose in the UK and Whole Foods Market in the USA (aka “Whole Paycheck”) can bob along comfortably in a cost-of-living crisis even as hard discounters like Aldi and Lidl (Aldi is the fastest growing grocery chain in the USA) nip market share from middle-of-the-market chains. In the UK, “Which” Consumer Choice magazine’s 2024 survey of customer satisfaction with grocers shows M&S and Aldi in the top 2 positions and Asda and Morrisons in the bottom 2.

Big and small branded food companies have had their challenges as shoppers have leaned more to purchasing private label products. Smaller brands have struggled to get on retail shelves as grocers trim their ranges to increase efficiency. “Shrinkflation”, i.e. reducing the size of a product whilst maintaining the same price, has become pervasive not least in confectionery. International cocoa prices have tripled over the past 3 years and our favourite choccy bars have quietly lost weight! Don’t forget food service, too – many consumers are eating out less or focussing on value meals which, in themselves, may have shrunk in size (e.g. there’s fewer Burger King chicken nuggets in a box than pre-2022). Are consumers giving up treats to save their money? NO – in a stressful world, many want “delightful distractions” and one trick is to include in the ingredient list for your product an item which has a guilt-removal health halo – “oh, look, it’s got those blueberries bursting with antioxidants in it (<1%)”!

Back at the farm level, fresh food producers – meat, eggs, dairy, fruit & vegetables – have had a particularly torrid time this past 3 years. Fresh foods are the competitive standards for grocery retailers and mainline supermarkets price matching hard discounters is ubiquitous. It’s galling for fresh produce growers to read that “In time for Easter, (hard discounter) Aldi Lowers Pricing on 7 Staple Vegetables To Just 15p Each” and premium retailer Waitrose “Commits To Good Health by Slashing Prices Again On Fresh Vegetables” – particularly so because most of the principal retailers aren’t backward in coming forward to advise food shoppers that they have close commercial relationships with their “farmer partners”! Normally circumspect in criticising their major customers, UK grower groups have shrieked foul play leading to a “Farm to Fork Summit” back in May 2023 in the UK, a Senate Select Committee Enquiry on Supermarket Prices in Australia (February 2024) with AUSVEG calling for action to secure fair prices for suppliers and there’s been similar calls for regulatory action across The Tasman Sea in New Zealand. Farm groups seek strengthening of instruments such as the UK’s Groceries Supply Code of Practice (GSCOP). The fact of the matter is that improved GSCOPs are useful for improving suppliers’ bargaining position with major customers but additional action by food producing business is required. This will be for discussion in our next mini blog! For fruit & vegetable producers, the double whammy has been that, in the cost-of-living crisis, consumers in the UK, EU, USA, Australia (amongst others) have reduced their fresh produce purchases to conserve dwindling real household income.

In the UK, a combination of some poultry/egg/meat/horticultural farmers stopping production because of, inter alia, negative margins (e.g. cucumber growers not planting at a loss because of escalating energy costs, import competition, and sticky retail prices), escalating input prices for feed (well, for everything!), and extreme weather conditions (e.g. a super abnormally wet and warm 2023/24 Winter), have led to the unwelcome sight of empty shelves in grocery stores. Back in November 2022, most of the major UK grocers rationed egg purchases. In mid-April, tomatoes are few and far between on UK retail shelves because of extreme weather conditions in our out-of-season source countries of Spain and Morocco. This has focussed attention on whether the UK nation is sufficiently food secure (and, concomitantly, farm input secure for energy, CO2, fertiliser, etc.).

Give or take, the UK is about 60% self-sufficient in food, and 75% self-sufficient in “indigenous” food (i.e. the food we can grow in the UK as we’re poor at growing bananas!). In history, we’ve been at 100% (pre-1750’s), under 40% (early-1950s) and up to 65% (mid-1980s). The level of sufficiency is, largely, a function of government price support and trade protection for agriculture (e.g. deficiency payments to farmers in the 1950s, followed on by EU payments from 1973). In February 2024, our Prime Minister announced the establishment of a Food Security Index reflecting the nation’s concern about food availability in an uncertain world threatened by global political instability and climate change. Whether this translates into additional protection for UK food producers it’s too soon to say. Politicians of any stripe must balance the interests of domestic food producers and consumer voter food budgets. But, in a global warming world and the rapid advancement of high tech horticulture (e.g. advanced hydroponics and vertical farming), we’d be surprised if the current low level of UK self-sufficiency for vegetables – 53% – and very low level for fruit – 16% – doesn’t increase substantially through time.

So, once we’ve sorted current supply chain problems and the cost-of-living crisis recedes will it be balmy times for UK and, indeed, global agriculture? After all, the farmers of the world should be on a pedestal: in 1954, the global population was 2.7bn and most were fed; by 2024, our world population is 8.1bn and most of them are fed …. by farmers using the same, even less land than in 1954. Astonishing! But, this Herculean agronomic effort has come with adverse consequences that are contributing to climate change and biodiversity loss. We can see this locally (e.g. David lives by the River Wye polluted by agricultural runoff) and internationally (the Amazon region lost a rain forest area 3 times the size of the UK between 1985 and 2021).

We know the size of the climate change problem and the consequences of inaction. Wise Benjamin Franklin opined “Don’t put off ‘til tomorrow what you can do today”. What’s more, through the series of UN Climate Change Conferences (the COPs), responsible (most) nations have already made promises/commitments on limiting the global temperature increase to 1.5C above pre-industrial levels, and 16 other world sustainable development goals (UN SDGs). We’re way behind delivering on our promises. In COP28 (Dubai, Nov/Dec 2023), however, most countries signed up to a “Declaration on sustainable agriculture, resilient food systems, and climate action”. So what? Just UN yabbidy yah? Our children/grandchildren won’t thank or forgive us if we sit on our thumbs. In the next 2 COPs (late-2024 and late-2025), we’ve committed to move from vision to firm action plan on agriculture and food by the end of 2025 with targets such as: cutting greenhouse gas emissions by 25% and halving N2O and CH4 emissions from agri-food systems compared to 2020; and ensuring global agri-food systems are net carbon sinks by 2050. None of this is easy but, what is certain is that farmers of our world must be in the vanguard driving change in how we produce food for our growing world. This isn’t agri-politics, it’s a fundamental requirement for the continuing existence of our planet! We’ve got to change our food production practices and, likely, our diets. There’s no messing with the forces of nature and let’s give polar bears bigger beds!

David Hughes and Miguel Flavián

April 19th, 2024